Biofuels M&A: 2025 Review & Outlook

Editor’s Note: For quite a number of years, we have been pleased to collaborate with our friends at Ocean Park Advisors to bring you an annual report for Biofuels Mergers and Acquisition activity during the year — and the trends and takeaways therefrom. Here is this year’s edition.

By Ocean Park Advisors

Special to The Digest

It was a split year for biofuels merger and acquisitions (M&A) in North America. Ethanol activity remained steady, although only two operating ethanol plants changed hands aside from The Andersons’ buyout of their partner. There was minimal interest in biomass-based diesel (BBD), with only one non-operating biodiesel (BD) plant sold and no renewable diesel (RD) M&A transactions. Uncertain biofuels policy, shifting tax incentives and margin pressures limited M&A. Instead, ethanol companies invested in ethanol decarbonization, including carbon capture and sequestration (CCS) and plant efficiency projects. In the BBD sector, overcapacity of the refinery-owned RD plants deflated margins. RD continued to displace BD gallons, leading to distress especially in independent BD producers that are not integrated to feedstock. In the past, operators bought non-operating biodiesel plants to re-start them. Recently, they’ve scrapped or repurposed them, cutting overall biofuels production capacity.

Overall, six operating ethanol plants, including two non-operating ethanol plants and one non-operating biodiesel plant, totaling 781 million gallons per year (MGPY) of capacity changed hands in six deals in 2025.

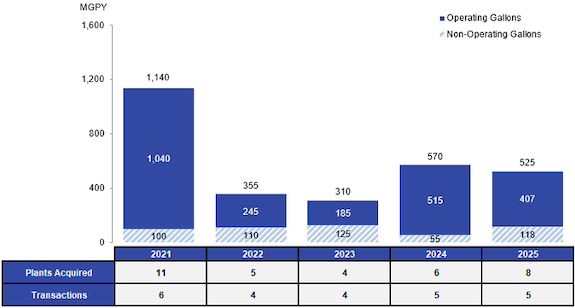

2025 Ethanol M&A

North American Ethanol M&A: 2021- 2025

Source: Ocean Park analysis.

Note: Excludes minority ownership transactions. 2025 ethanol M&A volume of 525M gallons reflects the incremental 237M gallons acquired. by The Andersons.

Six operating and two non-operating plants traded in 2025. The five transactions involved eight plants with a combined capacity of 525 MGPY. Notably, there were two large-scale, non-distressed M&A transactions with valuations far exceeding $1.00 per gallon.

- The Andersons bought the remaining 49.9% ownership interest in The Andersons Marathon Holdings (TAMH), its joint venture with Marathon. The Andersons added 250 MGPY of ethanol production capacity through a $385M purchase (excluding $40 million of working capital), which represents a $1.54 per gallon valuation. The transaction included four ICM plants located in Albion, MI; Clymers, IN; Greenville, OH; and Denison, IA, and increased The Andersons’ total ethanol capacity to 475 MGPY, making it the fifth largest U.S. producer.

- POET acquired Green Plains’ Obion plant. As part of its strategic review process to optimize its plant fleet, Green Plains completed the sale of its 120 MGPY operating ethanol plant in Obion, Tennessee for $170M at a $1.42 per gallon valuation. The proceeds were used to retire the company’s mezzanine debt, strengthen its balance sheet and enhance overall liquidity. The sale reduced Green Plains’ total production capacity to 783 MGPY, across nine ethanol plants. Green Plains remains the fourth largest ethanol producer in the U.S.

- TorTrax acquired Attis Ethanol. The 100 MGPY plant was idled after a fire in 2022 and sold at auction. Attis originally purchased the facility from Sunoco in 2019 to pursue cellulosic fuels. TorTrax, a family-owned holding company, is redeveloping the Fulton, New York site into an industrial campus.

- E. Innovation acquired Agri-Energy from Gevo. A.E. Innovation acquired the idled 18 MGPY ethanol plant located in Luverne, Minnesota from Gevo. A.E. plans to restart production as a demo plant.

- Turnspire Capital acquired ICM Biofuels. Turnspire acquired the 50 MGPY ethanol plant located in St. Joseph, Missouri, along with the LifeLine Foods ingredient business. Turnspire, a New York-based private equity firm, completed its first ethanol-sector acquisition.

Instead of ethanol producers selling their production capacity, they are reinvesting and allocating that cash towards CCS, Carbon Intensity (CI)-reduction, efficiency projects and/or plant expansions, thereby putting a damper on available assets for buyers. Under the One Big Beautiful Bill Act (OBBA), the 45Z tax credit of up to $1.00 per gallon provides ethanol producers with a significant economic incentive through year-end 2029 to lower their CI scores. Tier 1 ethanol plants with direct-inject CCS capabilities are monetizing tax credits and will continue to command premium valuations. For example, Gevo sold $52 million of 45Z credits for 2025 production by sequestering CO2 into the well at its North Dakota plant.

For individual ethanol plants without onsite storage capacity, carbon capture pipelines present an alternative means of unlocking CCS and generating 45Z tax credits by transporting compressed CO2 from multiple plants to geologic sequestration sites where they can inject and bury the CO2 forever. In October 2025, Tallgrass Energy placed its $1.5 billion Trailblazer CO2 pipeline into service which spans 392 miles across Nebraska, Colorado and Wyoming. Tallgrass wholly funds the construction and connection of its Trailblazer CO2 pipeline and splits the 45Z economics with the ethanol producer. To date, Tallgrass has entered into agreements with approximately 11 ethanol plants. Several Nebraska ethanol producers have already begun capturing and transporting CO2 via the Trailblazer pipeline, including ADM (Columbus), Green Plains (Central City, Wood River and York) and Mid America Agri Products (Madrid). Ethanol plants with operational CCS projects, either through on-site sequestration or via pipelines, generate significant incremental cash flow and therefore will remain prime acquisition targets.

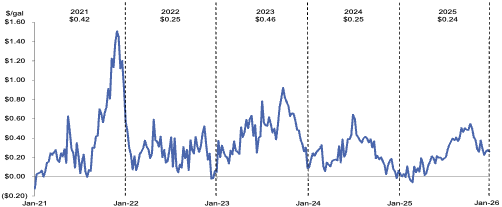

The U.S. ethanol industry is driven by relatively inelastic, policy-driven demand and a supply base prone to overcapacity, with margins fluctuating based on corn costs, co-product values, energy costs, blending economics and increasingly, CI scores. The market is supported by Renewable Fuel Standard (RFS) blending mandates (mostly E10), although higher blends like year-round E15 and E85 are significant opportunities for future growth. While 2025 ethanol production likely hit a record high of 16.3 billion gallons, domestic demand remains slightly below pre-pandemic levels due to stagnant gasoline consumption. Ethanol exports, which are a critical factor for supply-demand balance, are projected to exceed 2 billion gallons in 2025, another all-time record. According to Iowa State University, ethanol EBITDA margins averaged $0.24 per gallon in 2025, supported by record exports and emerging carbon markets.

US Ethanol EBITDA Margins: 2021 – 2025

Source: Iowa State University, Center for Agricultural and Rural Development (CARD).

Historically, low margins boost ethanol M&A – distressed assets become cheaper, and well-capitalized strategic buyers pounce to increase scale, diversify operations and realize synergies. Conversely, high margins set higher expectations on asset valuations, which can also spur deals but usually at premium multiples well in excess of $1.00 per gallon. With the recent trend of CCS and related carbon monetization, margins could swell further based on these new 45Z and 45Q credits which could in turn increase transaction values in the ethanol segment.

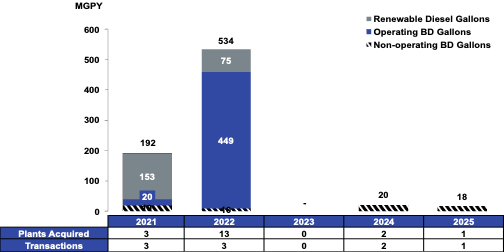

2025 Biodiesel & Renewable Diesel M&A

NORTH AMERICAN BIODIESEL & RENEWABLE DIESEL M&A, 2021- 2025

Source: Ocean Park analysis.

Note: Based on transaction closing date.

After the Chevron / REG transaction in 2022, no operating biodiesel and renewable diesel plants have traded. In 2025, there was one transaction involving a non-operating plant with 18 MGPY of capacity.

- Hamilton Oshawa Port Authority (HOPA Ports) acquired World Energy / Hartree’s biodiesel facility. HOPA Ports, a Canadian port authority, acquired World Energy / Hartree’s 18 MGPY idled biodiesel plant in Hamilton, Ontario. HOPA ports is actively searching for a suitable partner to operate the facility.

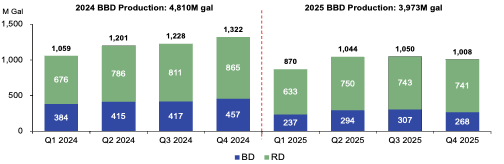

Biomass-based diesel had a rough 2025: falling volumes and negative margins. In 2025, total U.S. BBD production fell 17% year-on-year to nearly 4 billion gallons.

US BBD Production: 2024 and 2025

Source: EPA.

Both BD and RD production margins were largely negative. Diamond Green Diesel, the RD bellwether jointly owned by Darling Ingredients and Valero, generated a loss of $0.02 of EBITDA per gallon in Q3 2025 compared to a gain of $0.25 EBITDA per gallon in Q3 2024, with total RD production decreasing by 26% during this period.

Renewable Identification Number (RIN) oversupply, weak Low Carbon Fuel Standard (LCFS) prices and the expiration of the Blender’s Tax Credit (BTC) drove producers to curtail production, idle plants, repurpose capacity or restructure.

The number of operating BD plants in the U.S. has declined each year since 2020. Integrated soy crushers dominate the small, shrinking sector, leaving a handful of independents. As a result, buyer appetite remains limited, and M&A is largely distressed-driven. BD production, which fell to a five-year low, experienced a pronounced year-over-year decline of 34% to 1.1 billion gallons. Multiple independent BD plants idled their operations last year including FutureFuel, Western Iowa Energy and Western Dubuque. In addition, Hero BX, which previously operated four BD plants with 130 MGPY of capacity, entered receivership in June 2025 and was marketed for sale through a court-ordered process although no buyers have emerged.

RD production, which accounted for 72% of total BBD production in 2025, fell 9% year-over-year to 2.9 billion gallons. Developers are delaying or shelving plans amid prolonged margin weakness. Notably, Cargill exited its RD joint venture with Love’s, underscoring the pullback in development activity. CVR Energy also announced plans to convert its 100 MGPY RD unit in Wynnewood, OK, back to hydrocarbon processing, due to higher soybean prices and the BTC expiration.

Sustainable Aviation Fuel (SAF) M&A and Announcements

There was one transaction in 2025 involving process technology.

- Conestoga Energy bought SAFFiRE Renewables from Southwest Airlines, including IP and technology to convert corn stover into low-CI ethanol for SAF. Conestoga plans to co-locate SAFFiRE’s pilot production facility at its Arkalon ethanol plant in Liberal, KS, and is expected to be operational in 2026.

Total U.S. SAF consumption in 2025 was only 250 to 300 million gallons, less than 2% of total jet fuel use. Domestic SAF production capacity more than doubled with new plants coming online, including Phillips 66’s conversion of its Rodeo, California refinery and Diamond Green Diesel’s SAF / RD plant in Port Arthur, Texas. However, SAF is pricier than conventional Jet A fuel – often two to five times more – due to its limited availability, capital-intensive technology, and higher feedstock costs which necessitates policy support and presents a significant challenge for airlines that operate on tight profit margins and seek costs comparable to Jet A.

Despite the small market, capital investments continued last year. Notable announcements include:

- Calumet / Montana Renewables announced a big expansion of its SAF plant in Great Falls, Montana from 30 MGPY to 300 MGPY, with an initial build to 150 MGPY by mid-2026. It previously closed a $1.4B DOE-guaranteed loan in January 2025. The loan guarantee is structured in two tranches, with the first tranche of ~$782M now funded, with the remaining balance available as a delayed-draw facility through full construction completion in 2028.

- LanzaJet’s Freedom Pines Fuel Facility in Soperton, GA, became operational in November 2025. The $300M plant uses ethanol as feedstock and has 10 MGPY of SAF production capacity.

- GEVO announced its 30 MGPY SAF alcohol-to-jet project in Richardton, ND located adjacent to its recently acquired low carbon ethanol plant and CCS facility.

- Par Pacific, Mitsubishi, and ENEOS formed Hawaii Renewables, a JV to produce renewable fuels in Kapolei, HI, in July 2025. Mitsubishi and ENEOS invested $100M for a 36.5% stake. Once operational, the facility will be capable of producing ~61 MGPY of RD/SAF/naphtha (~60% SAF).

- New Rise Renewables commenced SAF production at its 38 MGPY plant near Reno, Nevada in February 2025. The facility can pivot between SAF and RD production without the need for equipment or process modification.

North American Biofuels Outlook for 2026

Regulatory

Regulatory uncertainty around biofuel mandates and blending rules shaped dealmaking throughout 2025. The Inflation Reduction Act (IRA), which shifted federal tax incentives from the Blender’s Tax Credit to the 45Z Clean Fuel Production Credit, was followed by the One Big Beautiful Bill Act (OBBBA) and not enacted until July 2025. In addition, the U.S. Environmental Protection Agency (EPA) delayed finalizing RFS blending quotas for 2026 and 2027 until Q1 2026. Such policy ambiguity created headwinds for M&A activity, slowing potential transactions as buyers await clearer demand signals and sellers awaited opportunity to unlock further value for their assets. In the meantime, industry players are making strategic investments to reduce their carbon intensity and seeking to monetize carbon credits.

The U.S. biofuels sector is entering 2026 with strong long‑term policy support (i.e. RFS, OBBA, LCFS), but there is some short‑term uncertainty around rule finalization, tax credit guidance, and trade policy. These factors shape investment decisions, feedstock markets, and the pace of industry consolidation.

- In June 2025, the EPA proposed RFS volume increases for 2026 and 2027 but has delayed finalizing the mandated volumes until Q1 2026.

- Total Renewable Volume Obligation (RVO) targets were raised to ~24B RINs in 2026 and ~24.5B RINs in 2027 (up from ~22.3B in 2025), with most of the growth allocated to advanced biofuels and biomass-based diesel.

- The proposed BBD category rises to ~7.1B RINs in 2026 (vs. ~5.4B RINs in 2025), while conventional ethanol remains flat.

- In addition, the EPA floated a new domestic vs foreign RIN value adjustment. Imported biofuels and foreign feedstocks would generate discounted RIN value, favoring U.S. production.

- Regarding Small Refinery Exemptions (SREs), the EPA cleared nearly the entire backlog of 140 SRE petitions from 2016-2024, removing uncertainty around actual obligated blending volumes.

- EPA’s supplemental proposal would reassign only ~50% of RINs waived under SREs, permanently lowering future obligated RIN demand, while more than 2.5B RINs tied to past SREs are expected to re-enter the market, creating a near-term oversupply of credits and muting the impact of higher future RVOs.

While the regulatory environment underwent a major overhaul following the passage of OBBA, industry stakeholders are still awaiting final rulemaking. In early February 2026, the U.S. Department of Treasury and IRS released proposed regulations for the 45Z Clean Fuel Production Credit, initiating a 60-day public comment period that closes on April 6, 2026. OBBBA previously extended the duration of 45Z by two years through 2029, providing much-needed longer-term certainty for capital improvements. As proposed, it also restricts eligibility for 45Z to qualifying renewable fuels from feedstock produced or grown in the U.S., Canada or Mexico starting in 2026. This effectively curbs the use of imported used cooking oils or foreign grains from receiving tax incentives, giving U.S. corn oil and soybean producers a massive competitive advantage. In a major win for corn ethanol, there is no longer an Indirect Land Use Change (ILUC) penalty, which previously inflated CI scores and now makes it easier for ethanol plants to qualify for federal tax credits. In a blow to the SAF industry, OBBBA reduced the value of the SAF tax credit from $1.75 per gallon to $1.00 per gallon to be at parity with other clean transportation fuels like RD.

Ethanol

The ethanol industry remains focused on lowering CI scores through a combination of CCS, process modifications, and examination of energy inputs to maximize credit values. Many producers are also continuing to pursue capital projects that increase production and/or diversify product profile while reducing operating costs to bolster their competitive positions. Ethanol plants with operational CCS projects, either through on-site sequestration or via pipelines, will remain prime acquisition targets. The 45Z economic benefits from OBBA have increased owners’ expectations on value and created potential financial tailwinds for the industry. There have been fewer announced sell-side processes as many M&A discussions are bilateral, prompted by active buyers. Legislatively, President Trump is working with Congress to pass a bill finalizing year-round E15, which if enacted, will boost ethanol producers and corn growers.

BBD

The BBD sector faces challenging market conditions. Diamond Green Diesel, for example, cut RD production year-over-year and reported a financial loss in Q3 2025. Nevertheless, RD continues to grow its overall share at the expense of BD, driven by integrated oil companies focused on meeting compliance obligations. The prior surge in new RD capacity flooded the market with advanced biofuels RINS and LCFS credits, keeping margins in negative territory. Policy is still up in the air (i.e. finalization of 2026 and 2027 RVOs and impact of retroactive SRE approvals) so BBD producers do not know when they will make money again. More producers could idle or shut down in 2026. Liquidations or distressed sales of independent BD plants in particular could be common in 2026, although there are currently no buyers in this environment. Recent auctions and sales for distressed assets failed to drum up significant interest. When the dust settles, buyers might emerge.

Conclusion

The biofuels M&A market was bifurcated in 2025. Ethanol assets with CCS or low-CI feedstocks remained attractive, while the BBD sector lagged amid policy uncertainty, margin pressures and supply-demand imbalances. RD has continued to push out BD gallons, leading to distress especially among independent BD plants not integrated to feedstock. RD production is dominated by the refiner-owned obligated parties who need compliance credits, but most plants are not operating at full capacity. The nascent SAF sector continued to attract significant investment but not acquisitions. The long‑term trajectory of the renewable fuels sector remains positive as demand for biofuels expands in the U.S. and globally, but regulatory clarity and policy support will be a key catalyst for M&A activity in 2026 and beyond.

About Ocean Park

Ocean Park is a leading boutique investment bank focused on industry segments across the agricultural supply chain including the ag inputs, renewable fuels and chemicals, energy, food, and AgTech sectors. The Ocean Park team has significant operational and transaction experience, including advising on mergers and acquisitions, financings and restructurings. Since its founding in 2004, Ocean Park has successfully completed over 80 transactions and client engagements, including over 40 biofuels transactions. Its office is in Minneapolis, MN.

This material is solely for informational purposes. The information in this document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security or to provide any investment advice. Any securities are offered through Ocean Park Securities, LLC, a member of FINRA and SIPC. Ocean Park’s professionals are licensed registered representatives of Ocean Park Securities, LLC. For more information, please visit oceanpk.com or call (310) 670-2093.

Category: Thought Leadership, Top Stories